Improving financial capabilities by developing digital skills

In March 2015, Lloyds Bank published its second UK Business Digital Index highlighting the various factors contributing to the slow move towards becoming digital for a significant portion of SMEs. Last week, the first UK Consumer Digital Index was launched, establishing the link between digital and financial capability and investigating It found that £3.7bn of online savings for consumers could be made if the digitally and financially excluded were to realise online opportunities.

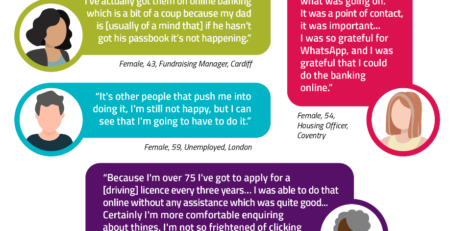

The research was carried out on the basis of a survey of 1 million Lloyds bank customers and on quantitative research involving individuals currently not using (either because they do not want to or are unable to access) a standard bank account.

The report found that 11.1 million people in the UK have low digital capability (they are unable to access online information and services, and therefore missing out on the opportunity to compare prices on a large scale and to make additional savings). Of the highly digitally capable, 9.9million people have low financial capabilities (i.e. less likely to manage an unplanned financial event and to achieve financial resilience). However most UK consumers (31.1million adults, 61.5%) are both highly digitally and financially capable.

The research also analysed the benefits of high digital and financial capabilities on mental health and concluded that “being digitally capable helps consumers’ financial resilience and enables a greater feeling of wellbeing???.

Compared with the findings of UK Business Digital Index, regional differences aren’t significant in terms of digital and financial capability, although interestingly, the Index reveals that London, has the highest numbers of consumers but also the highest number of consumers with low financial capability. Age was found to be a key factor in determining the frequency of and internet attitude towards internet use. For the over 60s, worries about privacy and security, lack of motivation to gain digital skills are examples of drivers for digital exclusion.

The accessibility to an internet connection was not identified as a barrier to online banking. The authors of the report called for Digital and Financial stakeholders to work together to promote access to welfare and online services, to raise awareness of online tools. The FinTech industry has a key role to play in developing innovative products and services to meet the demand of the low digital and financially skilled, and that Generation X (40-49 year olds) should be mobilised as Digital Champions to pass on their skills to other generations.

The full report is available here: http://www.lloydsbank.com/banking-with-us/whats-happening/consumer-digital-index.asp